Spotify (Part II) – A great product but a bad business?

Some investors view Spotify as a great product but a bad business. CEO Daniel Ek said as much himself at their recent investor day:

“You [investors] think that Spotify is a great product with a great experience. But some may also think that we’re a bad business or at least a business with bad margins for the foreseeable future.”

While there have been many zombie companies that raised capital over the last few years with questionable economics, Spotify is not one of them. In this post I’ll lay out Spotify’s pricing power and why profitability should increase meaningfully, which I believe should result in a much higher valuation.

1) Pricing Power - Long tail of price increases to come

In my previous post, I highlighted that the existence and growth of Spotify as clear evidence of pricing power, as Spotify’s product is one of the key reasons why society began paying for music again. Furthermore, in 2020/21 we also saw some more recent and tangible evidence of Spotify’s pricing power as they launched wide scale price increases (up to 20%) across over 30 markets, including key regions like the UK and the US. Despite this, churn continued to decrease over the period and Spotify continued to grow subscribers.

Spotify’s Family Plan (6 users, 1 subscription) has been the largest contributor to growth over the last few years and is also responsible for reducing churn given its lower price point and increased stickiness (i.e., painful to cut a plan when 5 of your friends/family are using it). In my view Spotify’s Family Plan is significantly underpriced, with users getting monthly access to the world’s music and podcast libraries for less than the cost of a cup of coffee. The Family Plan is also >70% cheaper than the Individual Plan across most of Spotify’s markets.

Spotify’s Family plan has been a great product to drive adoption and increase stickiness while they have been in land grab mode. However, given the value they provide users and the current pricing of the product, I believe there’s significant opportunity for price increases in this plan, especially across developed markets. In my view Spotify can increase Family Plan pricing by at least 2-3x over the longer term, while still remaining cheaper than the Individual Plan.

We have already begun seeing higher prices flowing through the industry. Apple Music increased their US Individual and Family prices by 10% and 13% in October 2022, while Amazon Music recently increased their prices by 11-20%. This leaves Spotify in a great position to also increase prices going forward.

2) Low margin but still has internet-like economics

A key issue investors have with Spotify is its low gross margins. While Spotify is an internet business, it sells access to media which will always represent a significant portion of the cost of goods sold - resulting in lower gross margins. Low-gross margins are generally looked upon unfavourably by tech investors. However, in Spotify’s case, the low-margins are mostly optics. Would the fundamentals of the business change if Spotify reported a Net Revenue figure instead? (i.e., Revenue less Royalties). Despite the low margins, the business still has internet-like economics as it is highly scalable and relatively capital-lite. A great way to visualise this is to look at Spotify’s cumulative financials over the last few years.

Despite generating losses of €3.3b since 2015, Spotify has generated €1.3b in Free Cash Flow due to the capital-lite nature of the business.

Conversely Netflix - who enjoys much higher gross margins than Spotify (Netflix 40% vs Spotify 26%) - has burnt a cumulative $7b in cash over the same period despite generating profits due to the capital intensity of the business.

These charts above highlight the platform-like scalability of Spotify’s business model, despite being a media business. As I highlighted in the previous post, Spotify differentiates on all things non-content while the SVOD players solely compete via content differentiation. Constantly having to create hero content in a high-churn industry is capital intensive and carries more risk, as much of their financial performance (i.e., sub adds) is driven by the success of said content.

Content differentiation in the music streaming landscape is not a viable strategy due to the fragmented nature of music supply (from an artist perspective), which inherently lends itself favourably to an aggregator like Spotify. We saw this playout in 2017 when several artists began promoting Tidal, a competing streaming product.

Case Study: Got 99 Problems but Tidal ain’t one

In 2017 Jay-Z removed his music catalogue from Spotify in an attempt to nudge listeners onto Tidal. Tidal was owned by Jay-Z and several other artists including Rihanna, Beyoncé, Jack White, Kanye West, Usher, and Madonna. Over the years several of the artist/owners began launching albums and songs exclusively on Tidal in an effort to increase its user base. Despite this, Tidal failed to gain traction and Jay-Z eventually returned his full catalogue back on Spotify in 2019.

While some of Spotify’s users would have been disappointed that Jay-Z’s content was no longer on the platform, the abundance of substitute products (i.e., rap songs from other artists) and Spotify’s leading user experience kept users on Spotify. Content exclusivity failed to create a competitive advantage due to the fragmented nature of music consumption.

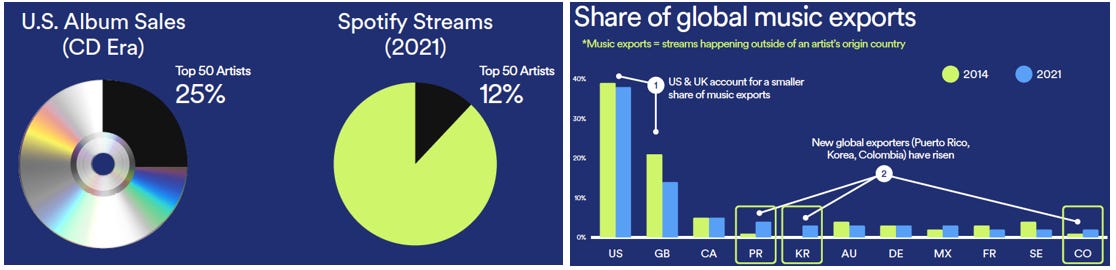

Fragmentation in music consumption continues to increase. In 2021 the top 50 US artists accounted for 12% of total Spotify streams, whereas during the CD era the top 50 artists accounted for 25% of CD sales. We are also seeing increased geographic diversity of our listening habits with countries like Puerto Rico, South Korea and Colombia becoming major exporters of music. The increased diversity of society’s listening habits will only strengthen Spotify’s market position over the long run.

3) Profitability is going to increase . . . a lot

Spotify has never reported an operating profit. While part of this was due to lack of scale in its early days, I believe this is mostly due to reinvestment in growth initiatives and market conditions that didn’t demand profitability from management teams. Spotify’s aggressive hiring has resulted in a significant degradation of their per employee efficiency metrics. Spotify’s gross profit per employee peaked in 2019 at €391k (US$430k) per employee. Since 2019 Spotify has increased its total headcount by 130% while revenue only increased by 73%, which has brought gross profit per employee down to €288k.

This is clearly unsustainable and management have made it clear to the market they intend to improve the businesses efficiency from 2023 onwards (i.e., recently reduced headcount by 6%). At Spotify’s current scale (c.€3b in gross profit), they are clearly more than capable of covering their core operating costs and generating profits, given ~49% of employees sit within R&D and R&D accounting for 47% of gross profits.

With a renewed focus on efficiency I think Spotify could comfortably generate more than €500k gross profit per employee, which will leave it in decent company relative to some peers/tech leaders below.

Another area where Spotify should deliver some efficiencies is within sales and marketing. Spotify’s subscriber acquisition costs have exploded over the last two years with sales and marketing spend per gross subscriber add up 44% since 2019. This is primarily due to increased investment in above-the-line marketing spend and non-music endeavours like advertising sales staff, podcasting, and sponsorships.

Given the renewed focus on efficiency, I believe we could see Spotify’s headline S&M per gross add return to pre-COVID levels of €11 per gross subscriber, which alone would drive ~400bps of margin improvement.

Final Thoughts

Spotify is the market leading audio platform that is driving adoption of audio streaming around the world. As of December 2022, 8% of the world’s population was a monthly active user of Spotify (ex-China, Russia). Spotify’s subscription adoption within its developed markets has increased 3-4x since 2016 with 15% of North Americans and 13% of Europeans paying for a monthly subscription. Over the long run, I expect 20-25% adoption of Spotify’s subscription service in its developed markets.

Spotify continues to remain free cash flow positive, with limited share-based compensation dilution. They are in prime position to continue to self-fund their growth ambitions and dominate the audio streaming market. While they are yet to generate a profit, the business is more than capable of delivering profits at their current scale, especially when considering they are overinvesting in R&D and Sales & Marketing (47% & 54% of 2022 gross profit).

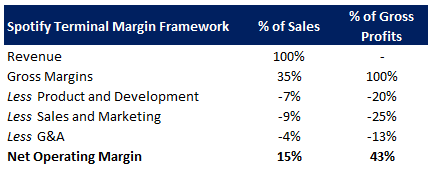

Assuming the above terminal margin framework - which I believe is achievable - I see a realistic likelihood that the business will increase in value by more than 2x over the next three years, assuming a 15x multiple. This valuation is not ridiculous when considering Netflix and Tencent Music at 23x and 14x.

There are a few risks I’d highlight with regards to the business case.

Macro - The advertising market is very weak and is expected to further deteriorate in 2023. I currently assume Spotify’s ads business falls 3% in 2023 (i.e., Impressions +20%, CPMs -23%), but this could prove too bullish in a tough macro environment which presents risks to my earnings and revenue forecasts.

Competition - Spotify needs to reinvest in product to maintain its competitive advantage and differentiation. I do not believe anyone will ‘out-Spotify’ Spotify, however there can always be new music distribution models which can present risks to Spotify. As we stand today, the current SaaS model of audio consumption seems well entrenched for the foreseeable future.

Operating expenses - While I have laid out a framework for Spotify to comfortably generate an operating profit, they have yet to generate profits and there is a risk that I have overestimated the scalability of the model or the efficiencies available within S&M and R&D.