AI, Web3, The Metaverse: Lessons from past technologies for investing in AI and the future

Lessons from previous technology advancements & Hype Cycles

Over the last few years, we've witnessed several massive technological advancements and Hype Cycles. Currently, AI is all the rage and I believe the hype around it is justified. AI products have the potential to transform our lives in significant ways, and it will be particularly disruptive for businesses.

However, this post isn’t about AI. In this post I will examine some of the significant technological advancements that we have seen over the last decade and share some thoughts on what lessons can be drawn from those technologies and Hype Cycles. These lessons can provide insights for investors on how to approach the AI revolution and future emerging technologies.

Mobile Internet (3G & 4G)

One of the most significant technological advancements over the last decade has been the mobile internet. The third (3G) and fourth (4G) generation of mobile networks gave utility to the mobile supercomputers that we now couldn’t live without.

The rise of the mobile internet spurred the growth of numerous industries, including social media, digital advertising, streaming, and the mobile economy at large.

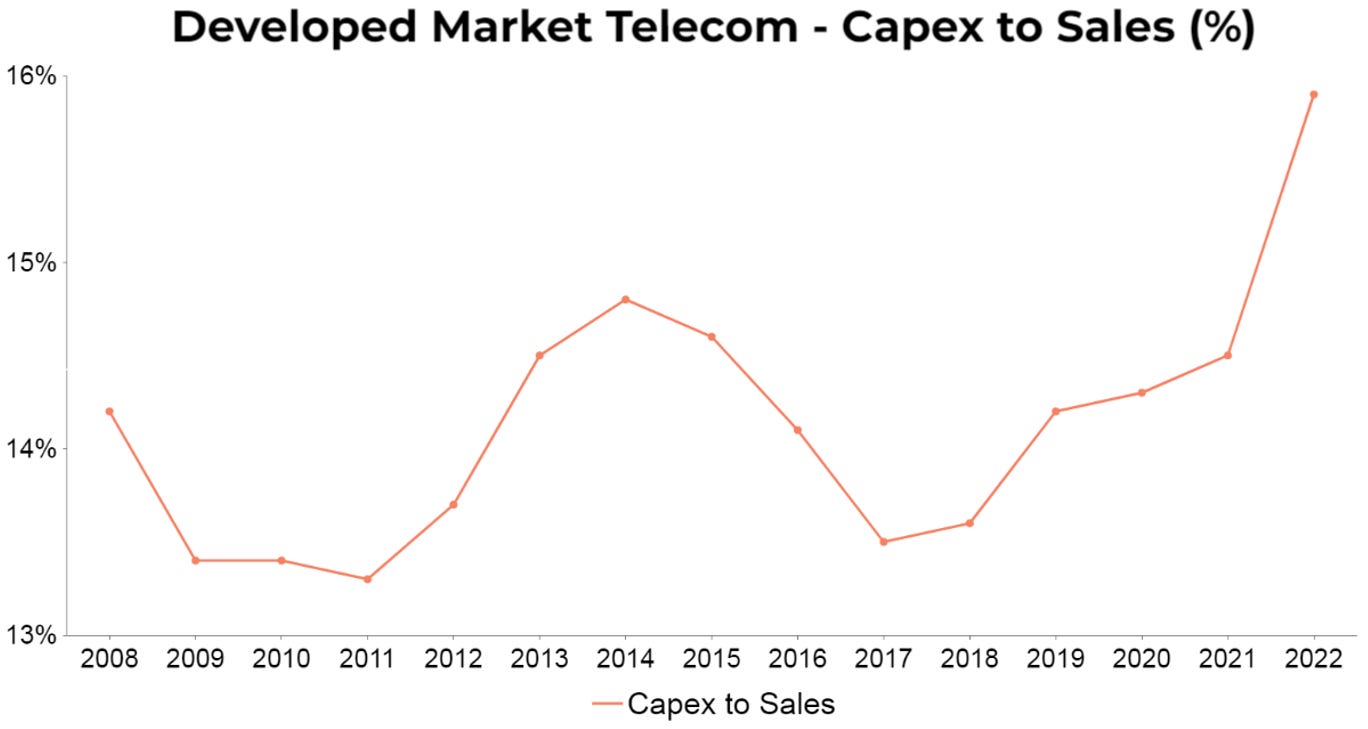

If an investor in the early 2000s possessed amazing foresight and recognized the potential of 3G/4G networks, where should they have placed their capital? An obvious bet would have been the telecom sector, as they owned and operated these highly valuable networks. This bet would have been logical.

In hindsight, it would have been one of the worst ways to play this thematic. While telecommunication companies built the networks that underpinned the mobile economy, they all failed to capture the economic activity that their networks enabled.

The above chart is pretty remarkable, particularly when you consider that telecom companies had first-hand insights into the structural trends taking place in society. They would have seen the explosion of mobile web traffic across their networks and would have seen which specific products were thriving (such as social media and streaming). Given these insights, one might assume that telecom companies would have been well-positioned to invest in (or create) Over-The-Top (OTT) and mobile internet products.

However, despite being at the forefront of the technological change happening within society, and somewhat responsible for it, telecoms failed to capitalise on it. As a result, the telecom industry has barely grown since the rise of the mobile internet. The businesses that captured the value from the explosion in the mobile economy were those that created new products and services that leveraged the mobile internet.

Cloud computing

Along with the mobile internet, cloud computing has been the other significant technological advancement over the last decade. Cloud computing has become the backbone of countless consumer and business products, ranging from video streaming to enterprise software. It is the infrastructure that has enabled the hypergrowth of companies like Airbnb and Uber, as they were able to achieve global distribution quickly and efficiently using the cloud.

Amazon Web Services (AWS) pioneered cloud computing in 2006. In a span of 10 years, AWS’ revenue has increased by >27x and now sits at $84b run rate.

Jeff Bezos received a lot of flak when he first launched AWS. Many investors would have preferred Amazon remain an e-commerce business. However, as we stand today, AWS is what has allowed Amazon to become one of world’s most valuable businesses, and it is the infrastructure that underpins most of the digital economy.

While AWS was established in 2006, it took close to a decade for the business to reach meaningful scale. Over that period there were plenty of customer testimonials, industry reports and feedback that investors could have assessed in order to determine AWS’ future success. Here are some instances of early customer testimonials and feedback on AWS:

Netflix became an AWS customer in 2009. Below is a testimonial from 2012 where they talked about the instant scalability and cost efficiencies that AWS provided.

Nasdaq adopted the cloud in 2008 to provide traders access to real-time market data. The cloud was a no brainer as it provided improved performance, quicker deployment and lower costs

Newsweek adopted the cloud in 2009 and reduced monthly operating costs by 75% while also retaining scalability during peak traffic events

Yelp migrated to AWS in 2014 to save costs and get new systems running in days, as opposed to months

Pinterest (2014) touted the benefits of AWS’ scale and speed, and the benefits of being able to focus on their product as opposed to underlying infrastructure

In 2014 Ticketmaster used AWS to reduce an applications costs by 80%

Amazon was AWS’ first customer and a great case study for AWS. They struggled to scale due to many of their internal teams building their own infrastructure for their applications, leading to duplication and higher costs. Amazon’s engineers eventually looked for ways to decouple their applications from their infrastructure, allowing for greater scalability, cost savings, and accelerated product development. This led to the creation of AWS.

While it took a while for cloud computing to become mainstream and investors were initially sceptical; the point I am trying to draw out is that there were plenty of publicly available studies, data points and customer testimonials which investors could have leveraged to understand the cloud. Gaining insight from the users of new technologies is crucial, and it is the most effective way to understand the value it offers.

Web3 / Blockchain / NFT

We all witnessed the explosion and subsequent collapse in the crypto / web3 industry over the last two years. The hype around crypto was extraordinary, with significant amounts of capital being deployed by both retail and institutional investors.

However, early on in the crypto boom, it became evident that there weren't many use cases for the technology. A few interesting perspectives that really stuck with me were those of the CEOs of ICE and Nasdaq. ICE was an early investor in Coinbase, while Nasdaq sells its exchange software to most of the crypto exchanges.

“When we look at the blockchain you can see it's version 1.0, the database is rudimentary compared to what we're doing. . . . It doesn't solve a lot of the major problems that we have . . . if you look at globally the interest in it and the investment going in . . . it's somewhat consumer-oriented” - Jeffrey Sprecher, ICE CEO

“We want to be on the forefront of making sure [our] technology is as modern as possible, bringing it into the cloud and allowing it to scale . . . But what I think is somewhat ironic is that the blockchain is meant to be a decentralized kind of trustless environment where buyers and sellers can actually find each other organically but every single crypto has been launched on a centralized exchange” - Adena Friedman, Nasdaq CEO

Both ICE and Nasdaq, two of the world’s largest exchanges, stated that their businesses had little use for the technology underlying Blockchain / crypto. The CEO of ICE basically said the only use case of crypto was to allow consumers to speculate on crypto. Investing in technologies without a clear use case is rarely successful.

What are some of the takeaways?

1) Speak to Customers and Users

This is the most important step when analysing any technology or product. Gaining insight from users of a particular technology allows you to determine the value it creates. Investors who took the time to speak with businesses that were early adopters of cloud computing would have had a better understanding of its growth potential. As previously highlighted, it was evident that cloud customers were reaping the benefits of increased efficiency (lower costs) and rapid deployment (higher revenue). Lower costs and higher revenue creates value in any business environment.

2) Avoid Hyped Technologies looking for a Use Case

Investors should be cautious when assessing emerging technologies that don’t have a use case. Investors should focus on the end-product and determine whether it provides any value. During a Hype Cycle there will inevitably be slick technologies that are overhyped but lack real world applications, just as we saw during the web3/crypto boom.

3) It’s not always the most obvious play: New Technologies might require New Products

The telecom companies spent billions building 3G & 4G networks, but they failed to participate in the incremental value created by those networks. This is because they did not create new products and services that would have leveraged the mobile internet. There is no guarantee that those companies closest to the technological advancements will benefit from said advancements.

4) It’s okay to be late

During a Hype Cycle, investors can feel pressured to deploy capital in any idea linked to that theme. However, it’s important to remember that it’s okay to be late. For instance, Amazon launched AWS in 2006 but they only began disclosing its revenue in 2015. An investor could have taken a decade to understand and gain comfort on the benefits provided by cloud computing and still made a 6x return by investing in Amazon in 2015 (or 6x in Microsoft the no.2 cloud player).

5) Look for Products, not Features

When evaluating new technologies that might have a single application, investors should ensure the single product can be monetized in a meaningful way and won’t end up as a feature within an established incumbent. (i.e., a slick calendar app is a feature, iOS/Android provides this feature for free).

6) Bet on innovative business leaders

Amazon was a leading online retailer but their innovation with regards to computing and infrastructure is what gave us AWS. Management quality is critical when evaluating investments, and backing management teams that are innovative, bold, and willing to pivot is a great strategy for investors looking to play a new technological theme.

7) Don’t be afraid to make mistakes: there are no Clean Sheets in investing!

Mistakes are a feature of investing, not a bug. We should take comfort that even the world’s greatest investors and businesspeople have made plenty of investment mistakes. Therefore, learning from mistakes, whether it be our own or others', is an important practice for all investors.

A critical error is to let previous investment mistakes scare us from betting on future technologies. Even if you do everything right - speak to all the customers, run the best financial models, understand the industry - there will be investments that fail. This shouldn’t discourage you: be bold, dust yourself off, and keep moving forward!